The federal reserve lowers interest rates and signals two more reductions the remainder of the year. At the same time mortgage rates are barely moving. Why are mortgage rates having such a large disconnect with the Federal Reserve. Will rates continue to fall or stay the same or higher? What does this mean for real estate? What good news is the chart above showing?

Federal Reserve does not control long-term rates

Although many believe that the federal reserve “controls” interest rates, this is a myth. The Federal Reserve can only set short term rates and the market “controls” long term rates like the 10 year treasury or 30 year bond. Long and short, the federal reserves moves are only part of the equation on long term rates. What is the “market” telling us of where rates head from here?

30 year bond predicts higher long term rates

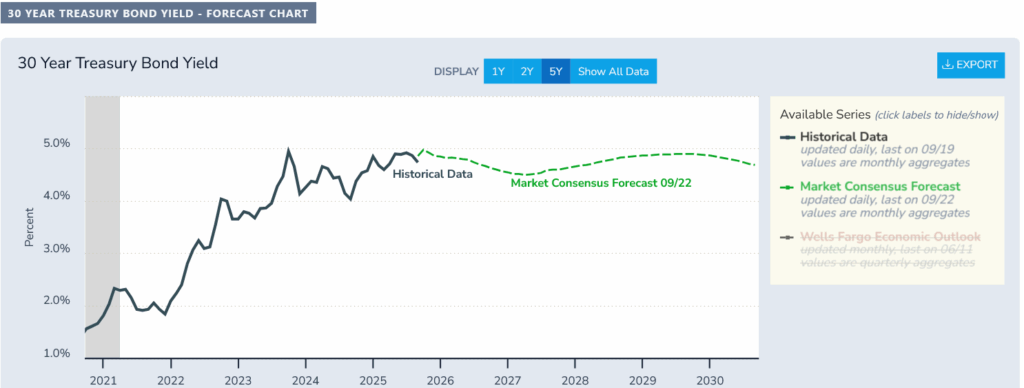

Although the 30 year bond is not the 10 year treasury that is basically the “peg” for mortgage rates, it does show the long term market expectations for treasuries and in turn mortgage rates. If we look at the chart above the latest predictions the bond market is predicting a small little dip and then long term rate will continue rising. The market could be making these predictions for various reasons:

- Inflation remains higher: This means that 30 year bonds would need to stay high/pay a premium to ensure investors real dollars continue growing

- Increased deficits: Increased deficits cause and increase in government borrowing leading to an increase in the supply of bonds. As supply increases, prices fall which leads to higher yields (remember treasury prices and rates work in inverse)

I would agree with the predictions above as there are considerably more factors influencing longer term bond yields to stay substantially higher for longer.

Mortgage rate predictions are wrong, they will be much higher for longer

If you look at any mainstream real estate publication, interest rates are predicted to fall well below where they are today. Unfortunately, I think these predictions are dead wrong. To determine where mortgage rates will be in 2026 if I lined up the 30 year historical chart above along with the historical mortgage chart below, it implies that rates will be very similar to where they were in 2008 which would put mortgage rates through 2026 in the 6.25 to 7% range which is about where they are now.

Even looking beyond 2026 rates likely will stay well above the ultra low rates from 2009 to 2019 as government spending ramps up which will keep rates considerably higher than the last 10 years.

What do 6% and above rates mean for residential and commercial real estate?

With rates staying higher for longer there will be huge impacts on real estate prices:

Residential: Higher rates eventually will lead to declining prices especially in higher priced markets as less people can afford to purchase expensive houses. Assuming a 500k mortgage at a 4% rate precovid the payments would be 2,387/month, now fast forward and that same mortgage would be 3160/month. This is an extra 9300/year in mortgage payments. This huge jump in payments does not work for most prospective buyers which will ultimately lead to prices falling in order to increase affordability. On the flip side, based on the lock in effect, the higher for longer will also lead to the residential real estate market basically “stuck” where it is with low volumes as borrowers cannot or will not give up their low rate.

Commercial: We have not even come close to seeing the bottom in the commercial market. As rates remain higher cap rates will also need to rise which will ultimately lead to a much deeper reset in commercial property values. Billions in mortgages are going to reset over the next few years and for now lenders have kicked the can down the road but as rates remain higher for longer eventually the market will have to face the music of much lower property values. For example, I’ve seen office buildings trading at 20-30% off their values from just a few years ago. You will also see a further reset in multifamily and retail as cap rates are way too low with treasuries staying higher for longer.

Summary

The market is dead wrong on the assumption that interest rates will rapidly fall anytime soon and “save” real estate. We are already seeing this play out today. Even with the recent cuts and predicted ¾% cut the remainder of the year interest rates are basically stuck. Unfortunately, larger government spending and the push for a soft landing leading to inflation will keep long term rates like mortgages much higher for much longer than is being priced in. This is clearly shown in the 30 year bond yield prediction above.

Since the market hasn’t come to terms with higher for longer, the market is grossly underestimating the impacts to residential and commercial real estate. With mortgage rates above 6% through 2026, commercial real estate is primed for a substantial correction as the current prices are not sustainable in a higher rate environment. For example, why would someone buy a commercial property on a 4-5% cap when they can buy a government bond with the same return with zero risk. Unfortunately, they would not, which means prices must adjust downward. On the flip side the residential market will continue either staying stuck or trending slightly downward.

Unfortunately predicting when the reset will occur is challenging as macro factors like a war, surge in oil prices, stock market meltdown, etc… can happen out of nowhere. With that said, my best guess is mid 2026 as the market comes to grips that low long term rates are not going to bail out the real estate market as rates stay higher for longer. On the flip side, we also could avoid a correction and basically kick along in a stagflationary economy for a while.

Additional Reading/Resources

- https://fred.stlouisfed.org/series/MORTGAGE30US

- https://econforecasting.com/forecast/t30y

- https://www.fairviewlending.com/fed-cuts-rates-why-are-mortgage-rates-rising/

- https://www.fairviewlending.com/commercial-real-estate-what-is-causing-the-decline/

- https://www.fairviewlending.com/root-cause-of-real-estate-price-declines/

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends . I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games).

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender