When I saw the headlines about NY reducing property insurance rates I was definitely intrigued. How can NY reduce property insurance rates 30% overnight while the rest of the country is facing double digit increases year over year? What is New York’s secret? Can NY serve as a roadmap for other states to greatly reduce property insurance rates? How has NY’s proposal worked in other states?

New York Plans to save money by eliminating profit on insurance policies

How will NY reduce insurance rates by 20-30%? By leaning on the city’s coffers, the insurance policies will be cheaper to issue because the government doesn’t have the same profit demands as private insurers, Bozorg said. And it will provide more options to buildings that might have more trouble securing an affordable insurance policy.

The whole plan is to have a government run insurance program that supposedly will reduce costs. Unfortunately this is not a new idea, CA has a state run plan along with Florida and now Colorado and in each case insurance rates have actually risen as opposed to fallen for the majority of property owners.

New York insurance plan is a transfer tax

Although our politicians want us to believe that money grows on trees and simply eliminating profit will solve all woes, the reality is far different. Let’s think about the US post office. It has not only eliminated profit for the last 20 years it has been operating at a loss that taxpayers are picking up every year. New Yorks insurance proposal will follow the same path. When profit is taken out of the equation the incentive for effective plans are also removed. You can see this in pretty much any government service from the TSA security to your local DMV. If these agencies were privatized they would operate considerably more efficiently and provide a better product.

The New York tax proposal is transferring huge amounts of risk from the private sector to taxpayers reducing incentives to mitigate risk. For example, a private insurance company would charge more for riskier properties, under the city plan everyone would get a break and I’m sure they will not charge the appropriate risk premiums because if they were they would not be able to undercut a competitive insurance market.

Before getting into how a government run insurance plan actually works in real life, it is important to discuss the issues that are causing insurance rates to skyrocket.

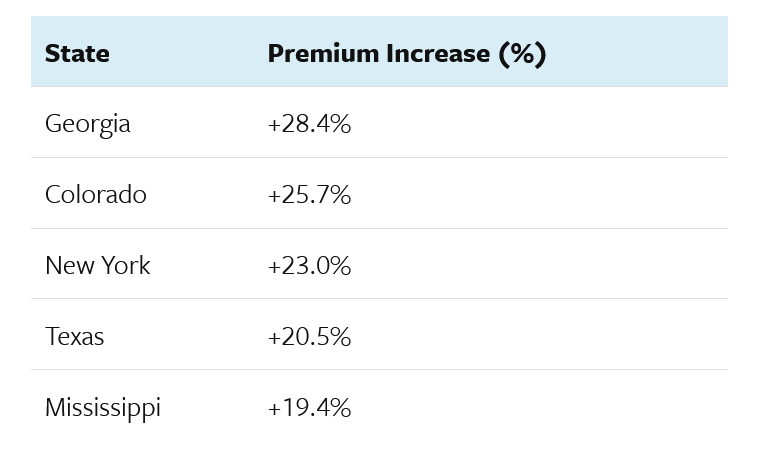

Why the huge jumps in property insurance costs throughout the country?

“People just aren’t aware that these natural disaster risks are occurring everywhere. It’s not just where the headline news points you to in terms of where natural disasters are occurring.” The report said the US was seeing an increase in the number and severity of natural disasters, including hurricanes, tornadoes, and wildfires which had “greatly increased the short and long-term risk for insurers and led to increases in insurance costs and reductions in coverage for property owners”.

4 reasons property insurance premiums are skyrocketing

There are four primary drivers of increased insurance risks throughout the country that are pushing premiums through the roof.

- New Risks of Fire: Look no further than the Marshall fire in metro Denver that burned suburban areas and the losses are now pegged at 2 billion dollars. Before the Marshall fire, the risk was deemed low in many metro suburban locations, the Marshall fire changed that equation and forced insurance companies to reprice their risk throughout the state.

- Increase in Hail claims: There have already been several major hailstorms in Denver this year, as costs increase from Hail and other hazards, these are passed on to homeowners

- Skyrocketing rebuild costs: Rebuild costs continue to climb from higher labor to material costs, to increase building requirements. For example, to install a new hail resistant roof is now 50% more than a conventional roof, but the impact resistant roof is now the code minimum in many areas.

- Increased building in higher risk areas: Along with increased losses, the amount of construction in high risk coastal, fire prone areas continues to increase which further increases the risk of losses to insurance companies.

Will property insurance costs continue to increase?

Yes! All of these risks look to only accelerate over the next several years which will unfortunately mean that insurance costs will continue to increase. At the end of the day, insurance companies have to be profitable or they will leave a market as we are seeing in California and Florida. This means that insurance companies must continue to increase their rates in order to remain profitable with the huge losses they are incurring in Colorado.

How will a city run property insurance plan play out in real life? A Cautionary tale from Florida

We can look no further than Florida for what happens with a state run program. Florida’s insurer of last resort, Citizens Property Insurance Corps., predicts to hit a record with nearly 2 million policyholders by the end of 2023, citing “continued instability” in the state’s insurance market.

According to the Citizens’ 2023 Operating Budget Report, the insurer ended 2022 at just above 1,153,000 policies and they predict to reach the highest number of premiums in their 20-year history by the end of 2023 with nearly 1.7 million.

The insurer averaged about 400,000 policyholders prior to 2020, when the state’s property insurance market started to crumble with several private insurers either going insolvent or pulling out of the state.

In essence the state insurance program has taken a substantial number of people out of the private Florida insurance marketplace and made it unprofitable for many insurance companies. Remember insurance is a volume game with the objective of taking in more from premiums than you pay out in claims. As the number of insured declines due to the state or a city subsidizing property owners, private insurance companies are no longer viable.

Summary: Can the government greatly reduce property insurance rates by merely eliminating profit?

New York’s plan to get into the insurance business is a bad solution to a problem that is not real. The overwhelming majority of property owners can obtain insurance at a price. The real reason that the state is getting involved in the insurance business is because property owners do not like the price of the new coverage. Remember, the price reflects the risk that insurance companies have and also creates incentives and disincentives in the market. Instead of addressing the actual risks, NY and many states are merely transferring the risk to taxpayers.

New York’s proposal is on a collision course with the insurance industry and we have seen how this has played out in California and Florida with mainstream carriers leaving the market which in turn has forced more into the state run program. The same will ultimately occur in NY leading to substantially higher rates for most property owners. When the dust settles insurance rates increase substantially due to less competition and also smaller pools by insurance companies to spread out the risk.

Unfortunately we are just at the beginning of the cost increases in the property insurance market. Look for more carriers to pull out in places like NY, Colorado, California, and FL with state/city run plans that will ultimately lead to higher rates for everyone else. To make matters worse, taxes will also have to rise for the subsidized insurance plans, remember money doesn’t grow on trees and economics is a zero sum game meaning someone will ultimately pay.

Additional Reading/Resources

- https://www.wsj.com/real-estate/new-york-mayor-mamdani-aims-to-cut-landlords-insurance-costs-62f79269?mod=hp_lead_pos8

- https://coloradofairplan.com/faqs/

- https://www.durangoherald.com/articles/colorados-wildfire-risk-is-so-high-some-homeowners-cant-get-insured-the-state-may-create-last-res/

- https://coloradosun.com/2022/12/30/colorado-property-insurance-wildfire-risk/

- https://coloradohardmoney.com/category/colorado-property-insurance/

- https://coloradohardmoney.com/why-are-insurance-costs-increasing-in-colorado/

- https://www.steamboatpilot.com/opinion/writers-on-the-range-its-a-perfect-storm-for-fire-insurance/

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends 😊. I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games). Learn how to find a reputable hard money lender and why Fairview is the best hard money lender for investors.

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender, residential hard money lender, commercial hard money lender, No doc real estate lender