For the last 4 years, credit scores have been artificially inflated due to the omission of student loans (and lack of payments of student loans) leading to huge gains in credit scores. Unfortunately this trend is set to reverse this year. Look at this chart above based on Transunion data, what does this mean for you? Why will the best scores get hit the most? What does this mean for real estate in 2025?

Why will credit scores be impacted now?

Before getting into the results of the study, it is important to refresh as to why credit scores will just now be impacted when the pandemic is well in the rearview mirror. When the Covid-19 pandemic hit in March 2020, then-President Donald Trump’s administration paused student-loan payments. While debt payments and interest accrual resumed in September 2023, borrowers were given a year to get back on track without missed payments showing up on credit reports. There’s an additional 90 days built into that ramp-up period, meaning that consumers who missed their October payments will see those delinquencies show up on credit reports for the first time in January of 2025.

What was in the TransUnion study on credit scores

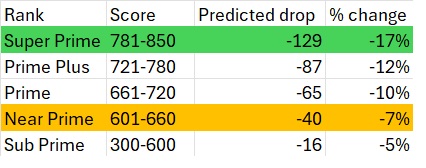

Super-prime borrowers — those with credit scores above 780 — who miss student-loan payments will see their scores slip 129 points on average, according to data compiled by reporting firm TransUnion. Look at the percentage change in scores from a missed student loan payment. The higher the score the bigger the impact. Based on the TransUnion data if someone started with a score of 780, a super prime borrower, and then miss student loan payments when they restart, the score could drop 129 points leading to a new credit score of 651. This score is now not even enough to qualify as a prime borrower.

How many people will the score drop impact?

Approximately 44 million Americans owe an outstanding student loan balance and nationally borrowers owe more than $1.7 trillion. While debt levels vary by degree and major, of particular concern are the nearly 4 million students who have dropped out of college without a degree but with student loan debt. Various studies have shown that between 5-7 million borrowers are in default. For the last 5 years these defaults had no impact on credit scores, but starting in 25 at a minimum five million will have their credit scores.

I would surmise that many of these score drops will be substantial as many stopped paying their student loans the last 4 years as they had an interest free loan from the federal government which will lead to a large number of borrowers with delinquencies when payments restart

What does the drop in scores mean for real estate in 2025?

Looking at the chart a huge number of borrowers will be impacted by the restarting of student loans. Any borrower that is super prime, prime plus, or prime will quickly drop to near prime or even subprime when student loan delinquencies are reported. The minimum credit score for an FHA government backed loan is around 620 and that assumes a higher down payment. Millions of borrowers will no longer qualify for conventional mortgages because of the score drop which will put pressure on real estate in 2025. This will be most profound in the middle income price points.

Impact to credit scores likely to be worse than the chart

How do I know the impact will be huge, I’ve seen hundreds of credit reports with trended data that show outstanding student loan balances with zero payments over the last 4 years and zero impact on the credit score. Essentially student loan borrowers have been getting an interest free deferment for the last 4 years to use the funds for other purposes.

Unfortunately, there is not an infinite cash flow for most borrowers that have student loans so making student loan payments takes cash away from something else, a car payment, a credit card payment, other disposable income etc… This means that the restarting of student loan payment reporting will hit borrowers hard and threaten their cash flow especially the middle class borrowers that are getting hit with stagnating wages, higher insurance costs, auto costs, etc… This will likely lead to more missed payments.

Cascading effects of a lower credit score

Although there is no doubt real estate will be impacted as less borrowers are able to qualify due to cash flow and credit scores, there are even bigger impacts. A lower credit score leads to higher interest rates on credit cards, a reduction in credit availability, higher car rates, higher insurance premiums, etc… These items will compound and make cash flow even harder for both prospective property owners and existing home owners. Ultimately we will see an uptick in foreclosures due to cash flow issues that have been hidden over the last 4 years.

Drop in credit scores impacts entire economy

Don’t underestimate the impact of student debt that now totals 1.7 trillion dollars. The federal government has essentially pumped billions of dollars into the economy by deferring student loans and borrowers had no incentive to make payments as there was no impact on credit scores and the interest was not accruing. Fast forward to 2025 and the piper will be paid.

Credit scores will drop and hundreds of thousands of borrowers will be impacted by this change. Real estate will be impacted as many homebuyers will no longer qualify due to cash flow with the student loan payments in the debt-to-income ratio along with reduced credit scores. The lower scores will have a cascading impact with less credit availability and higher payments on everything from auto loans to credit cards. We will see these impacts flow through in the 2nd and 3rd quarter of 2025 which will further hold back sales especially on mid priced homes.

Additional Reading/Resources

- https://www.bloomberg.com/news/articles/2024-12-02/missed-student-loan-payments-to-hit-super-prime-borrowers-harder

- https://www.fairviewlending.com/us-government-plans-to-unlock-850-billion-in-homeowners-equity/

- https://www.fairviewlending.com/car-loan-defaults-rise-what-does-this-mean-for-real-estate/

- https://www.ncsl.org/education/student-loan-debt-series#:~:text=Approximately%2044%20million%20Americans%20owe%20an%20outstanding,start%20a%20business%2C%20and%20save%20for%20retirement.

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends . I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games).

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender