What an insane 24 hours, a late night tweet on Tuesday announced the sudden firing of a Federal Reserve Governor essentially trying to eliminate the independence of the federal reserve while ensuring looser monetary policy. Ironically the opposite occurred and mortgage rates rose. What happens now? Above are the 5 likely scenarios that will play out in this event and there are opportunities and pitfalls with each scenario. What should you do now? What happens to real estate?

Is it legal for a President to fire a Federal Reserve Governor

While a president has never removed a Fed governor from office, one can do so for cause. Laws that describe “for cause” generally define the term as encompassing three possibilities: inefficiency; neglect of duty; and malfeasance, meaning wrongdoing, in office.

Why is President Trump firing Federal Reserve Governor Cook?

Cook’s firing stems from allegations made by Federal Housing Finance Agency Director Bill Pulte that Cook committed mortgage fraud. Pulte claimed in an Aug. 20 post on X that Cook had claimed two properties—one in Michigan and one in Georgia—both as her primary residence on loan applications. Pulte called on the Department of Justice to investigate Cook and said Trump had “cause to fire” her. He also wrote a letter to Attorney General Pam Bondi and Justice Department official Ed Martin on Aug. 15 alleging that Cook “falsified bank documents and property records to acquire more favorable loan terms, potentially committing mortgage fraud under the criminal statute.”

On the surface is sure sounds bad, but as you dig into it, the allegations are a mirage. When you are applying for a mortgage you select if you intend for it to be your primary residence. The way the current system is set up you can have multiple primary residence loans at the same time. For example let’s say someone was buying a house in GA with the intent to occupy it. After closing they step into the house and decide they don’t want to live there for whatever reason, they then keep the house as a second home with the same mortgage and buy another home or rent it or do whatever they want. There is no crime committed when people change their minds.

Remember the system is set up this way. If the government is concerned about the primary residence issue then over the last 30 years they could have easily updated the regulations to say that you can only have one government backed loan at a time. But they haven’t and instead they are using this supposed “mortgage fraud” as a heist to take over the federal reserve.

I’m going to step into some political hot water here and highlight that the Democrats are partly to blame for this. The Democrats during Covid began a huge politicization of the Federal Housing Administration ordering them to halt evictions, stop collections, and not allow owners who had rental properties backed by the government to collect rent. Long and short, the political takeover of Fannie and Freddie has been a disaster by both parties and has led us to where we are today.

What happens now with the Fed Governor firing on the line?

During the 08 crisis, I found it critical to use a variation of economic “game theory” to put probabilities beside events so I could best be prepared for whatever was thrown my way. The good news is you get to participate as well. Take the survey to the right and let me know your likely outcome and why. As this unfolds we will find out together what ultimately was the correct answer.

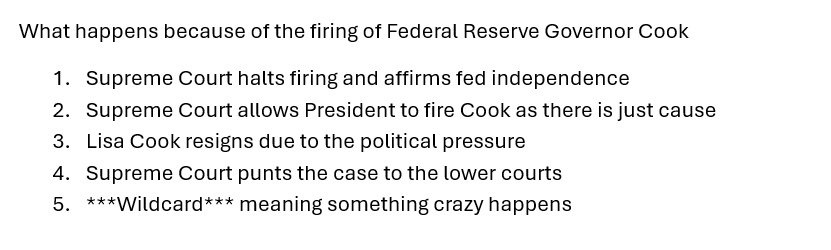

I made a simple decision tree of 4 likely outcomes and one basic wildcard (aka oh shit that nobody saw coming) and put probabilities by each one along with the likely impact on interest rates and the economy.

-

40% Supreme Court halts firing and affirms fed independence

- This would cause interest rates to go down both short and long term as market confidence is restored

- This is my hope and best case scenario, the irony is that this would also be the best case for the President as he would get the lower rates that he wanted.

-

30% Supreme Court allows President to fire Cook as there is just cause

- Short term interest rates would go down, but long term rates would skyrocket as the loss of confidence in the fed to fulfill their mandate on inflation

- Likely lead to a Stagflation scenario where interest rates rise at the same time consumer and business confidence falls. This would be a very bad outcome

-

15% Lisa Cook resigns due to the political pressure

- I don’t think this is a likely scenario based on the court cases so far but you never know

- If Cook resigns this would be similar to firing, might not be as bad, but the markets would interpret it similarly with a loss of Federal Reserve Independence.

-

5% Supreme Court punts the case to the lower courts

- I think this is a very unlikely scenario but you never know what might happen

- If this occurs, basically this whole decision could be stuck in the back and forth with the courts for quite some time which will lead to market uncertainty. This wouldn’t be the worst option but not a good one

-

5% ***Wildcard*** meaning something crazy happens

- In every decision there is always an unexpected OH SHIT! This could happen here as well. For example what if foreign countries got so scared about the US financial system that they severely cut back on their Treasury holdings leading to a huge surge in rates. What happens if someone else on the Federal reserve resigns or was pushed out? What happens if all the sudden there is a liquidity crunch in the treasury markets?

- There are a ton of what ifs that aren’t that far out there that easily could happen, as the saying goes when you play with fire someone is going to get burned. Although not a likely scenario, something bad could easily happen that could throw any models or predictions out the window.

What does all this mean for real estate the remainder of the year

Regardless of the outcome, real estate is going to struggle. Immediately after the President announced the firing Gold shot up and long term treasuries also increased. This points to a huge flight to safety/nervousness in the market. When Gold is in huge demand it means the market is extremely worried, this will ultimately flow through to consumer confidence. At the same time, the bond market via the 10-year Treasury is also worried about the future by increasing the risk premium demanded for longer term securities which means the market is worried about inflation. This flows through to higher interest rates. This could all work out, but I’m doubtful it will work out in time to save this year’s selling/buying season.

What should you do today?

You aren’t going to like my answer but like everything in real estate and finance it depends on your particular situation. For example let’s say you are closing on a house in 2 weeks, should you lock in a rate now? My answer for this scenario would be to let the market settle down and I would do the shortest ARM possible where the rate adjusts every month or two if possible as there likely will be a better opportunity for lower rates. On the flip side, if you are not convinced of a great outcome on one of the scenarios above then you might want to lock now. All in all, it depends on your risk tolerance. Furthermore, remember in every single situation there is always an opportunity, this recent development with the Federal reserve is no different, there could be some huge upside as well as huge possible downside.

Trump Fires Cook where do we go from here

The situation we are in is crazy. Before this week I had no clue who the fed governors were or where they lived or who they were appointed by or what mortgages they got or all sorts of random information. Suddenly, as a nation, we are living/ witnessing a real live Jerry Spring Episode!

The resolution of the Lisa Cook case is likely the biggest financial case in the last 100 years; since the founding of the federal reserve it has operated as an independent agency and this case threatens that precedent. Although during the Nixon administration he definitely “influenced” the fed to lower rates which led to a catastrophic economy over the years.

Regardless of your political bent or affiliation compromising the federal reserve’s independence will have far reaching consequences and will ultimately lead to higher interest rates and lower growth as everyone loses confidence that they will fulfill their mission of inflation fighting. Furthermore, this will lead to much higher growth periods and huge crashes as well. It is a terrible scenario.

The sad part is that this is all preventable. Remember our forefathers that created the constitution. The primary premise of the constitution after the Revolution was limited government. As the government keeps growing and growing this theory has been lost, leading us to where we are today. This has been done by both parties as deficits due to government spending continue to rise and the interaction in government in our every day lives continues at an unprecedented clip. I’m cautiously optimistic that the Supreme court will quickly squash this latest fiasco and hopeful for some upside but we are in wild times so it will be interesting to see how it all plays out.

Additional Reading/Resources:

https://www.fairviewlending.com/the-war-on-landlords/

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends . I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games).

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender, residential hard money lender, commercial hard money lender, No doc real estate lender