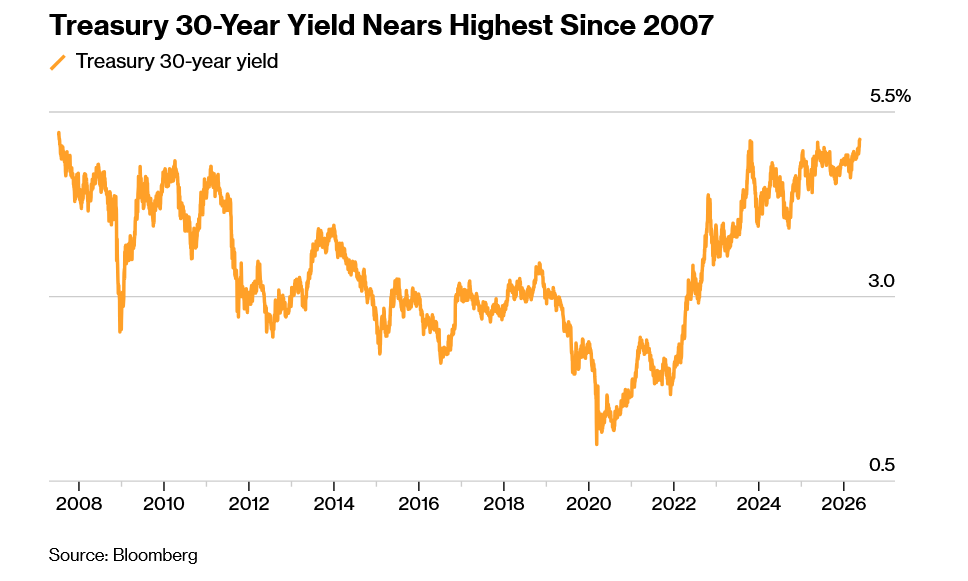

Look at this chart above, out of nowhere yields have made a U-turn with long term treasury yields surge to almost 20-year highs and predictions exceeding 6%. This is exactly the opposite of what economists had predicted at the beginning of the year which was quickly falling rates and subdued inflation. Why are they suddenly rising? Is this just a blip or is something larger happening in the economy? How does the surge in rates impact real estate prices? Is the real estate market at an inflection point?

Why are longer term treasury rates rising so quickly?

Global bond yields have surged in recent weeks as a jump in energy prices caused by the Iran war adds to inflationary pressures and compels central banks such as the Fed to consider raising interest rates. Add in worries over US budget deficits and signs that the world’s largest economy remains resilient, and the result is that investors have been seeking greater compensation to own longer-maturity debt.

Is this surge in rates a blip or a trend?

The million-dollar question is what happens next with rates. Will inflation quickly abate after the energy shock or has something else happened in the economy? There are two schools of thought on what happens next.

- Inflation is a blip: the market is currently pricing in a Goldilocks scenario where inflation rapidly decreases due to a resolution of the energy crisis. We are seeing this as stocks continue to power higher in light of rising rates.

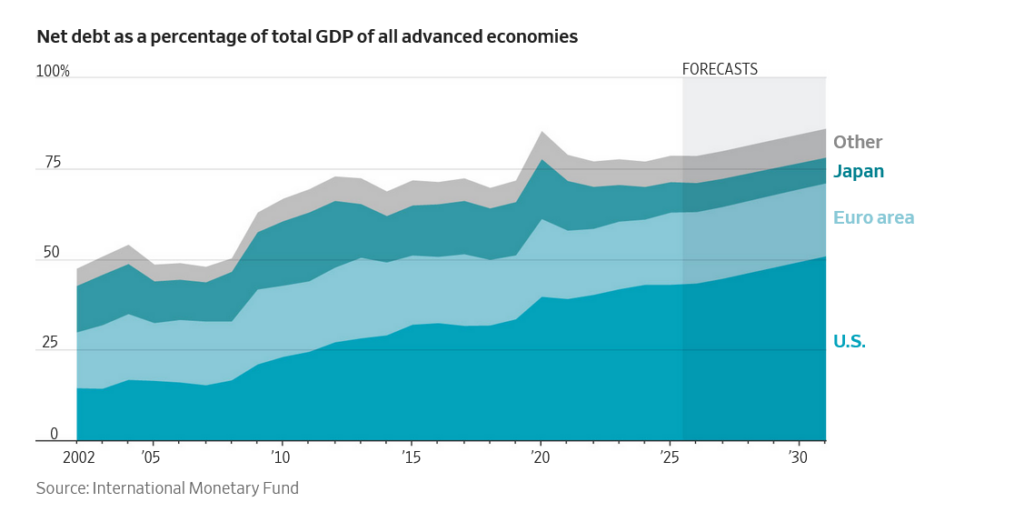

- Bigger structural economic changes leads to higher inflation: The bond market is pricing in the polar opposite scenario as we can see from the surging long term bond yields. The theory is that the economy is doing much better than expected while at the same time surging governmental debt is creating a structural issue with substantially higher rates for longer due to more supply of bonds. Look at the chart above of the surging national debt throughout the world.

Why care about bond yields when valuing real estate?

Economics is based on opportunity costs. You could buy X or Y and get a return for each asset, so it is a balance of risk and reward for investors. For example you could buy a government bond at 5.5% with basically zero risk or you could buy a commercial piece of real estate. Essentially as bond yields increase returns on other assets like commercial real estate must rise to compensate for the same risk of inflation. This return on investment in real estate is known as the capitalization rate (more details below) A good example would be a retail location that might have traded at a 4% cap rate in 2020 when yields were around 2%, the cap rate would now need to be about 2% higher than treasuries for the increased inflation risk which puts the cap rate around 6-6.5%.

What is the capitalization rate?

The capitalization rate (also known as cap rate) is used in the world of commercial real estate to indicate the rate of return that is expected to be generated on a real estate investment property. This measure is computed based on the net income which the property is expected to generate and is calculated by dividing net operating income by property asset value and is expressed as a percentage. It is used to estimate the investor’s potential return on their investment in the real estate market. In essence the cap rate is a measure of the “riskiness” of a property. A higher cap rate would deem a property more risky and a lower cap rate would mean the property is low risk.

Furthermore the Capitalization can also be considered the “trade off” rate for various assets.

How does the Capitalization rate impact commercial real estate values

To value commercial real estate you can look at what comparable properties are selling for and also calculate the net operating income to determine the value. The income approach is critical to the valuation of a property. The basic calculation is Net Operating income (revenues-expenses and excludes mortgage/interest payments). The NOI is then divided by the capitalization rate to determine the value. For a basic example, lets assume a properties NOI was 100k/year and that the property was a high quality property so the cap rate was 5%, so the value is 2m.

Huge changes in commercial real estate values due to rising yields

There are two primary variables impacting value of commercial properties, the net operating income from the property, and the expected return on the property (cap rate).

- NOI (Net Operating Income): the income on many properties is declining substantially due to the virus. For example, the lease rates on office space are plummeting due to lack of demand, furthermore existing office users are negotiating lower rent rates to continue their lease. On top of this vacancy rates are ticking up as companies close or substantially scale back. Furthermore NOI is getting compressed due to higher inflation increasing the costs of just about everything from insurance, materials, labor, utilities, etc…

- Cap rates: Cap rates are surging as properties that were once deemed “safe” are now very risky, for example a restaurant in a great location might have traded on a 4 cap, now that property might trade on a 7 or 8 cap due to the uncertainty in the industry

A real-life example of the impact of Capitalization rates

Change in Cap rates: Assume a restaurant pays 100k/year in rent and it is a triple net lease, when the property was bought, a 4 cap was used, with the changes, now the cap rate has increased to 7 or 8 percent. The original value was 2.5m, now the value with a 7 cap is only 1.4m

Change in NOI: Assume the same restaurant now renegotiates the lease by 20% due to the surging costs of food and their loss in income which decreases the NOI to 80k which means they can’t afford the current rents. Now assuming as above the increase to a 7 cap, the value is now 1.1m.

What happens in real life is that NOI is typically reduced at the same time capitalization rates rise which leads to a double wammy for property owners. We can see this playing out in almost every office market throughout the country with some office properties values plunging to 50-60%.

What does the surging yield mean for commercial real estate values/defaults

There is going to be more pain ahead in commercial real estate. As rates continue to rise along with cap rates values will have to adjust. Furthermore many properties with higher cap rates and lower net operating incomes will not make sense except at greatly reduced prices.

On the flip side excellent properties with great tenants will still be in demand albeit at higher cap rates than today. The theory is that hard assets like real estate can act as a hedge against inflation as rents can be adjusted to compensate for the increased inflation.

Residential real estate values will also be impacted

Although the primary focus of this blog is on the commercial side, residential real estate will be impacted as well. We will see this first in large funds focusing on rentals that are already pulling back from the residential market as interest rates rise, costs rise, and income falls. From a true investment perspective many residential real estate properties no longer make sense for funds.

On the flip side, residential will be a bit more insulated than commercial properties because most residential mortgages are long term fixed loans (30 years) so there is not a constant need to refinance and if someone can’t sell their home, more often than not, they have the option to just sit tight.

Where do we go from here in regards to prices and cap rates?

The market has so far mis interpreted the extent of inflationary pressures coupled with increased government spending which is leading to the dangerous economic cocktail we are seeing today. In turn, the commercial real estate market and to some extent the residential market is in for a tough ride in 2026 and beyond as net income is reduced and cap rates are increased. This is just the beginning as there is considerable uncertainty as to how deep the income losses will be when leases come up for renewal and how substantial the cap rate increases will be due to higher long term rates.

Regardless of how this all shakes out and when there is more downside risk than upside heading into the second half of 2026; with that said, there might be some buying opportunities later this year and into next year as the market digests the new realities of higher interest rates.

Additional Reading/Resources:

- https://www.bloomberg.com/news/articles/2026-05-19/us-yields-flirting-with-2007-highs-entice-and-divide-investors?

- https://www.wsj.com/articles/see-how-the-global-government-debt-binge-is-rippling-through-markets-cb9ce3ca

- https://www.fairviewlending.com/cap-rates-increase-impact-on-real-estate/

- https://www.fairviewlending.com/what-the-latest-inflation-upsurge-means-for-the-mortgage-market/

- https://www.fairviewlending.com/is-stagflation-dead-what-happens-now/

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends 😊. I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games). Learn how to find a reputable hard money lender and why Fairview is the best hard money lender for investors.

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender, residential hard money lender, commercial hard money lender, No doc real estate lender