Look at the chart above of consumer delinquencies? We are now in line with 2017, but is that the real story? Look at 07 what do you notice? Will the economy mirror the 08 reset or has something else fundamentally changed? With the current delinquency rates are we like 03, 07, or 2017? What is the best guess for when a reset occurs?

The importance of delinquency tracking

As we can see with the chart delinquencies follow a pattern, they typically start small and rise over time, look at starting around 06/07 we saw delinquencies begin to rise modestly and then pick up huge momentum with a peak around 2010. Essentially we got an indication of what was to come with the rising delinquencies 4 years before things got bad.

On the flip side, look at 03, delinquencies rose and then fell again before rising substantially after 06. Essentially there was around a 7 year period before delinquencies hit their peak but only about 5 years before the official recession in 2008.

Long and short, we don’t know where we are in the cycle.

This cycle is different than 08 for three reasons:

Mark Twain famously said that history rhymes but does not necessarily repeat. Today’s cycle is much different than 08

- Don’t have the subprime exposure: the trigger for the 08 crisis was the subprime crisis where anyone with a pulse could get a loan, defaults rose which ultimately led to a market meltdown. We do not have that same risk in this cycle as underwriting is much stricter than in the past.

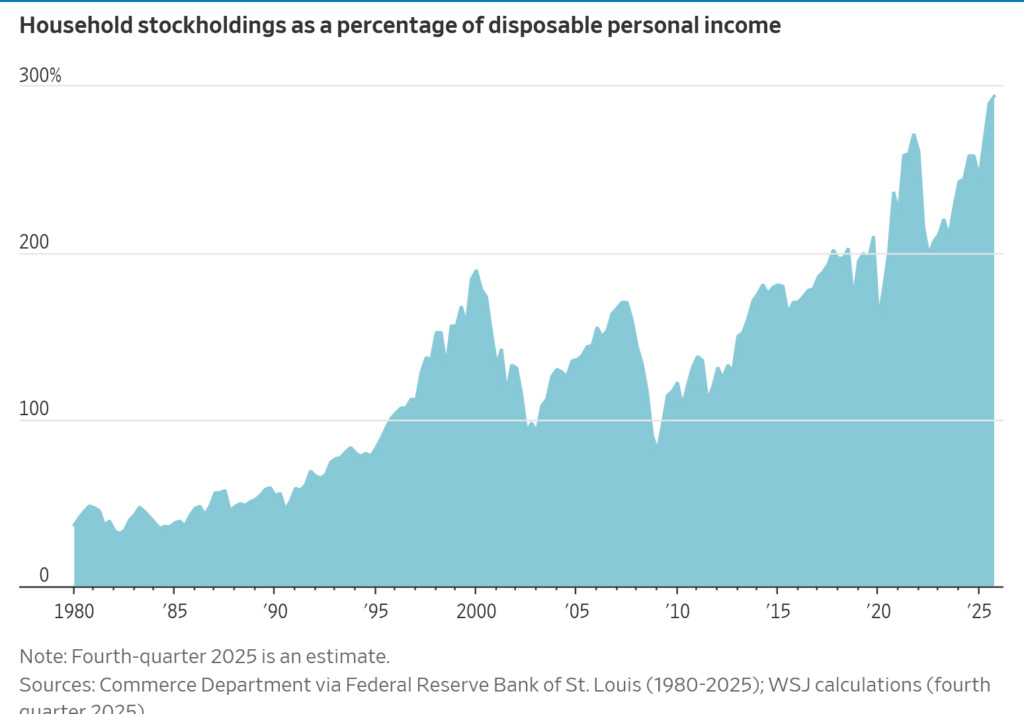

- Have a higher concentration in stocks: Look at the chart below. Today the stock market as a percentage of disposable income is double what it was in 2008. This means as the stock market pulls back from record highs, the wealth effect will trickle down and could easily lead to a major recession much quicker than 08.

- Debt today is higher overall than in 08: Today the amount of debt that consumers, businesses, and the government is at a record high. This means when things get rocky in the economy there is a much higher likelihood of much larger problems.

No big changes in the economy are imminent

Based on the charts above, there is huge uncertainty of where we head in the economy. To further the confusion, I surveyed readers and asked the question of what happens in the economy over the next two years. With a reasonable margin of error there are equal chances of basically every scenario from a huge crash to a roaring economy.

Big risk of when economy changes much worse

Although I can’t predict when the economic winds will shift, I am more concerned that we could have a much worse outcome than the markets are pricing in. Consumer debt, company debt, and government debt are all at records and defaults are increasing. We have seen in every cycle that somehow debt is the trigger. For example, in the last cycle subprime real estate debt was the fuse that lit the economic cannon leading to trillions in losses. This cycle, although mortgage debt via subprime lending is not as crazy as it was in 08 there are still risk factors.

For example, look at the federal deficit, there is no plan by either party to get debt under control which will lead to higher rates on everything due to more bonds for sale. Furthermore, there is a ton of unsecured consumer debt like buy now pay later that has never been stress tested. Couple these debts with corporations that have been on a borrowing spree and the risks to the economy are amplified.

What does all the data say about the economy?

What happens next and when is the million dollar question. My gut says we are at the beginning of this next cycle. Referencing the chart above this would put 2026 similar to 2006/7, but remember the worst impacts did not occur until 2010 which means we could still be several years away from the peak in the next cycle.

Although I don’t know exactly when the economy will reset, it does give me comfort that the survey results from a month or so ago also expressed huge ranges of opinions with equal chances of basically every probability occurring. Regardless of when the cycle starts, the huge increases in debt and the uptick in lates/defaults is a warning that the economy could change swiftly.

I liken our economy to a ship that is grossly overweight with debt and it could take on water at any time when the seas become choppy. Now is the time to prepare; I would implore everyone to reduce debt to ride through the storm and ensure you have a life jacket, aka ample cash, to ride through whatever storm the economy throws.

Additional Reading/Resources

- https://www.bloomberg.com/news/articles/2026-02-10/us-consumer-delinquencies-jump-to-highest-in-almost-a-decade?srnd=homepage-americas

- https://www.fairviewlending.com/what-will-be-the-average-30-year-rate-in-2026/

- https://www.wsj.com/economy/jobs/capital-labor-wealth-economy-2fcf6c2f?mod=hp_lead_pos3

- https://www.fairviewlending.com/has-the-economy-lost-its-mind/

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends 😊. I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games). Learn how to find a reputable hard money lender and why Fairview is the best hard money lender for investors.

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender, residential hard money lender, commercial hard money lender, No doc real estate lender