I saw a recent ad for a Porsche electric Taycan that was less than 18 months old available for half of its original cost. What can this huge drop in prices over a short time tell us about an impending real estate problem? Why am I even looking at Porsche resale values? What property types are most impacted, and will it affect you? What property should you never buy at any price point?

Why am I even looking at Porsche resale values?

Porsche cars provide a unique perspective on the economy. It is the higher end of wealthy discretionary purchases but not out of reach for many wealthy like a Ferrari or Bently. By watching Porsche, it is an indicator of where wealthy consumer spending is heading.

What can the Taycan tell us about lease vs Buy?

The Taycan in the ad caught my attention. New it books out at 140k and this one less than 18 months later with only 6k miles was listed for 70k, half the original list price. On the flip side a similar Porsche 718 with similar specs over the same 18 months had only dropped about 15%. It should not be a surprise as technology in electric cars is changing so rapidly it is hard to justify buying a new Taycan to take a 50% hit in less than 2 years.

Condos across the country are facing an eerily similar situation

As I was looking at the details on the Taycan, a lightbulb went off that many condos could be facing a similar situation to the Taycan with huge drops in values due to rapid changes in the market. In essence, in many condos it may no longer be worth it to buy certain units at any price.

What is going on in the condo market?

Condominium owners across the country are facing a paralyzing problem: They can’t sell their properties because of a fast-growing and mostly secret mortgage blacklist. Don’t worry this is not some crazy conspiracy from the government. I’ve experienced this first hand on multiple condos in Georgia, Colorado, and Florida.

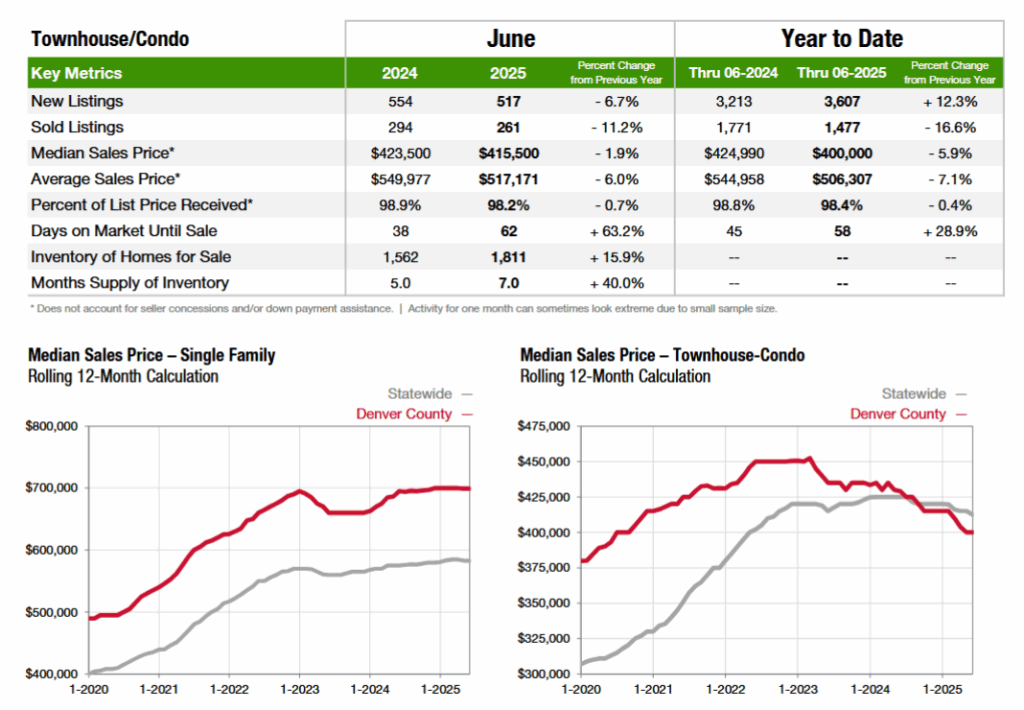

Look at the data above from 24 to 25 in Denver and you can see this beginning to play out with declining values and huge jumps in inventory up 33% year over year along with a decline in closings. This is a bad situation that is only going to get worse.

What was in the data on blacklisted condos?

The blacklist is maintained by Fannie Mae and includes condo associations that the mortgage finance giant thinks don’t have adequate property insurance or need to make critical building repairs. Being on the list can make it harder for potential buyers to get a mortgage.

The number of properties that fail to meet Fannie Mae’s standards has risen to 5,175 this month from a few hundred before Surfside.

Why the huge change in blacklisted condos?

Fannie Mae and sister organization Freddie Mac don’t make loans, but buy roughly half of the country’s home loans from lenders and package them to sell to investors, then guarantee payments on them. Loans that meet Fannie or Freddie’s underwriting standards, known as conforming loans, can be less expensive and require lower down payments than bespoke mortgages.

To ensure the debt can be repaid should the property be damaged or destroyed, Fannie and Freddie have long required a minimum level of insurance coverage for home loans they are willing to buy.

Last year, the firms issued clarifications of these guidelines, detailing policy no-nos that have prompted lenders to take a stricter line on insurance requirements, according to lenders, real-estate agents and insurers.

A spokeswoman for Fannie said its requirements are designed to “help protect borrowers from physically unsafe or financially unstable projects.” She disagreed with characterizing Fannie’s database of projects, which includes properties that both do and don’t meet its lending criteria, as a blacklist. She said the firm provides an online tool that allows lenders to check whether it accepts loans from a given project.

What two factors led to Condos getting on the blacklist?

There are two factors Fannie/Freddie look at to determine if a condo is suitable for financing:

- Maintenance/Reserves: After the condo collapse in FL a few years ago and new laws in many states, many complexes have found themselves severely underfunded for routine maintenance and expected expenses for roofs, foundations, elevators, hvac, etc…

- Insurance: Many condo complexes do not carry full replacement cost on insurance as required by Fannie/Freddie. One reason for the jump in insurance costs: Insurers now want to pay for the depreciated value of a damaged roof, rather than the full replacement cost, a feature Fannie and Freddie oppose. Many insurers also want to raise deductibles higher than Fannie or Freddie allow.

- A lot of associations are trying to reduce soaring insurance rates by agreeing to pared-down policies that can make their condos ineligible for mortgages backed by Fannie and Freddie. Some homeowners’ sales are falling through, and others are looking for buyers who can pay cash or get other types of loans.

- Shadow Ridge, a Los Angeles complex blacklisted in December, is in a brushfire zone but escaped this year’s infernos. Its homeowner’s association was recently quoted $2.6 million a year for a Fannie-compliant policy, 10 times the current rate, according to Jinah Kim, one of the board members.

What happens when a condo project is on the mortgage blacklist?

I’ve seen a few scenarios play out for condos that are unable to get conventional financing from Fannie/Freddie:

- Increase down payment: I’ve seen several occasions where a lender would accept the loan with a down payment of 30-35% as opposed to 20% or less depending on the lender. The issue is many of the complexes that have issues are affordable and borrowers can not afford a 35% down payment or they would be looking at a house or other property.

- Find another lender with higher rates: On a few occasions I’ve seen other lenders able to step in to finance albeit at higher rates.

- Can’t get financing: Some condos are unable to get financing at any level which leads to all cash sales

Regardless of which scenario above plays out, each one leads to much lower resale values. I’ve seen prices dropped from 10% to almost 40% if it has to be an all cash purchase. If you own a condo or are looking at a condo in a blacklisted complex financing will be more difficult and or could be non existent.

Some condo complexes will become basically worthless

I’ve seen this multiple times on condo complexes throughout the country where the units become basically worthless as the insurance and costs to update critical items outweigh the value of the units. This is especially true in lower priced condo complexes

Many low-priced condo complexes are no longer viable

Lower priced condo complexes will be hit the hardest as residents cannot incur huge jumps in dues needed for insurance and maintenance. This issue has been a long time coming as many complexes kept HOA dues as low as possible to assist residents but now, they have huge financial issues that have compounded.

Huge changes ahead in the condo market

It is unfortunate that many lower priced condos are no longer viable. Historically, someone could buy a condo, build some equity and then move into the single-family market. Now with house prices jumping throughout the country while condo prices are slumping the ability to move up is quickly being erased.

Summary

It is crazy, on the cover of the article is a Porsche that books at 140k which is a starter condo in many markets. Unfortunately, the market in electric cars and condos has shifted on a dime where it is no longer viable to buy a lower priced condo as the risk from special assessments for maintenance and insurance make the financial calculation perilous. Just as we see in the electric car market, it is substantially cheaper to lease as opposed to buy, that same equation is now true for many lower priced condos regardless of how cheap they are compared to a single-family home.

The unfortunate part is that as the condo market changes, the path to home ownership is radically altered as the entry point to buy is now so much higher and so much farther out of reach for first time buyers.

Additional reading/resources

https://www.fairviewlending.com/property-insurance-rates-set-to-jump-by-50-why-and-who-pays/

https://coloradohardmoney.com/condo-prices-fall-throughout-colorado/

https://www.wsj.com/finance/regulation/condo-sales-home-insurance-crisis-a921362b?mod=mhp

We are a Private/ Hard Money Lender funding in cash!

If you were forwarded this message, please subscribe to our newsletter

Glen Weinberg personally writes these weekly real estate blogs based on his real estate experience as a lender and property owner. I’m not an armchair reporter/writer. We are an actual private lender, lending our own money. We service our own loans and own commercial and residential real estate throughout the country.

My day job is and continues to be private real estate lending/ hard money lending which enables me to have a unique perspective on the market. I don’t accept any paid sponsorships or ads on my blog to ensure accurate information. I’ve been writing this for almost 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, facebook, and other social media and forward to your friends . I would greatly appreciate it.

Fairview is a hard money lender specializing in private money loans / non-bank real estate loans in Georgia, Colorado, and Florida. We are recognized in the industry as the leader in hard money lending/ Private Lending with no upfront fees or any other games. We fund our own loans and provide honest answers quickly. Learn more about Hard Money Lending through our free Hard Money Guide. To get started on a loan all we need is our simple one page application (no upfront fees or other games).

Written by Glen Weinberg, COO/ VP Fairview Commercial Lending. Glen has been published as an expert in hard money lending, real estate valuation, financing, and various other real estate topics in Bloomberg, Businessweek ,the Colorado Real Estate Journal, National Association of Realtors Magazine, The Real Deal real estate news, the CO Biz Magazine, The Denver Post, The Scotsman mortgage broker guide, Mortgage Professional America and various other national publications.

Tags: Hard Money Lender, Private lender, Denver hard money, Georgia hard money, Colorado hard money, Atlanta hard money, Florida hard money, Colorado private lender, Georgia private lender, Private real estate loans, Hard money loans, Private real estate mortgage, Hard money mortgage lender, residential hard money loans, commercial hard money loans, private mortgage lender, private real estate lender, residential hard money lender, commercial hard money lender, No doc real estate lender